Why and How to Build a Research Org

every vertical SaaS company should be doing research

“When you see something technically sweet you go ahead and do it, and you argue about what to do about it, only after you have achieved success.”

Oppenheimer

In the emerging effort to make the full TAM of labor addressable via software and robotics, there is a growing appreciation for how complex the world actually is.

That complexity is not a reason to sit on our hands and wait for things to play out.

We are finally at a moment where there is enough understanding around how model capabilities intersect with data, RL, evaluations, and the broader vendor stack that ambitious organizations can begin to behave differently.

The strategies are increasingly legible. The vendor ecosystem has matured. Open-source models have proliferated. The infrastructure required to pursue durable advantage has now emerged.

And so the implication is fairly straightforward: this is a moment for concentrated research ambition in every vertical.

This is not to suggest that vertical SaaS companies should become labs, but instead the organizations most likely to define their categories from here will be the ones that treat research as a competitive advantage in their vertical. Durable advantages will not come from merely consuming frontier models. It will come from building the internal capacity to turn model capability into a science.

There is almost no better crop of companies to pursue this advantage in theory than current vertical SaaS companies at scale. The revenues, customers, and data they commandeer have been hard won. Now is the moment to parlay this into the future.

And so now is the time for vertical SaaS companies to develop research organizations that can turn model capability into a decisive advantage.

On Acquisitions

First, it’s important to realize that the current strategies around AI acquisitions have had far more to do with product organizations than research. This is far different from how the labs, data companies, and RL companies have assessed the problem.

While vertical SaaS has prized acquisitions for near-term revenue strategies, lab acquisitions have been built more around the underlying data recipes, harnesses, research, and ML talent inside of their acquisitions.

This is not meant to be a critique of acquisitions ad hoc. These have been valuable acquisitions for accelerating product roadmaps. I’m simply suggesting that most vertical SaaS companies, even following these acquisitions, have insufficient research impulses to create novel agents that endure in the face of base model pressure.

But this isn’t merely about a defensive strategy. There’s one question that matters:

Do you believe the TAM is all of human labor?

Ignore for a second all the secondary questions you ultimately jump to, including margin profile, competitive dynamics, commodity pressure, and the rest.

Do you believe that the TAM is all of human labor?

If the answer is yes, then the question for vertical SaaS companies is simple: how do you go about capturing it in your vertical? Can you create an organization that does not just benefit from favorable tailwinds from base models that others will thrive from as well, but become a company that dictates the frontier for your industry?

If the answer is yes, the payoffs are not merely SAM expansion, but a range of partners to help get you there. In other words, the EV of a competent research organization is extremely high from both a credibility and revenue perspective.

Let’s look right now at how the labs behave. Anthropic and OpenAI are both increasingly going to market with partners: Harvey, Rogo, Sierra, and a litany of others. What do all of these partners have in common? A research-centric approach to the problems they are trying to crack.

Right now, the labs primarily judge traditional software companies as consumers of inference internally. Start addressing the TAM of labor and paths begin to open up.

Who do the new wave of vendors like Applied Compute, data companies, and more try to target? Companies with a tractable vision around the future of work in their vertical.

What are the companies most likely to endure? Companies like ServiceNow, which consistently put out some of the best research around frontier capabilities, small models, and more.

The research arm of these companies is a feature, not a bug.

In short, there are a number of tailwinds that directly benefit organizations that think this way.

In this conception, the base mission of research organizations is to deploy an increasingly complex supply chain of vendors and partners to deliver frontier model capabilities that product and engineering teams can then commercialize. Human data, RL vendors, compute vendors, and I’m sure many more will continue to proliferate.

What are the best examples of these research organizations in vertical-ish markets today?

Three examples: Shopify, Ramp, and ServiceNow.

Ramp Labs is a particularly useful example. Look at the diversity of experiments that Ramp is running, everything from Excel experiments to RollerCoaster Tycoon. The benefit is twofold:

AI is ultimately a talent, data, and compute game. A range of experiments signals to each of these markets that the company is a credible partner on the AI frontier.

Compute markets are trending weirder. What’s the payoff from RollerCoaster Tycoon? An internal team that increasingly knows how to handle long-horizon tasks and model evaluation. What’s the payoff from Excel agent capabilities for a fintech company? That one should be obvious.

The goal of research for all of these organizations is not just to have fun. It is about developing an internal team, muscle, and ultimately a model capability analysis function that can increase the rate of commercializable products.

In many ways, it is no different than what every physical-world company of scale does. Physical product companies spend hundreds of millions on R&D.

The future of software is beginning to look similar, except with payoffs measured in trillions across the economy.

Where should the research organization live?

Should it be concentrated in product, engineering, data, or something else altogether?

While the specifics will differ by organization, here’s my unsolicited take: it should live as its own organization.

There’s at least one reason to frame it this way: the goals of research and other organizations diverge before they converge.

Product organizations are concerned with driving near-term revenue from customers by building and managing products with large uptake. Their time horizons and KPIs are built around existing products, with some portion of time spent on near-term new product opportunities.

Research organizations are primarily concerned with identifying longer-term moats and model capabilities that can be turned into durable revenue. Their concern is not solely near-term product capabilities, but instead on pulling the frontier forward by 12–24 months. With novel model research, data, and evaluations, their goal is to deliver transformational capabilities that can result in long-term durable revenue and products at a pace that other companies in the vertical cannot match.

Of course, in practice this is going to involve a great deal of collaboration, with all aspects of the broader company contributing to AI advancement and becoming increasingly AI-native.

A thriving organization should be managing SLAs with product to deliver better performance at lower cost on a recently launched product, while simultaneously advising product that it can launch a first-to-market product with a newly developed model capability.

Which brings us to the fun part of this piece: where do we start? After all, research should be focused on a tacit goal. So what should research teams actually focus on?

Model capability underlies roadmap

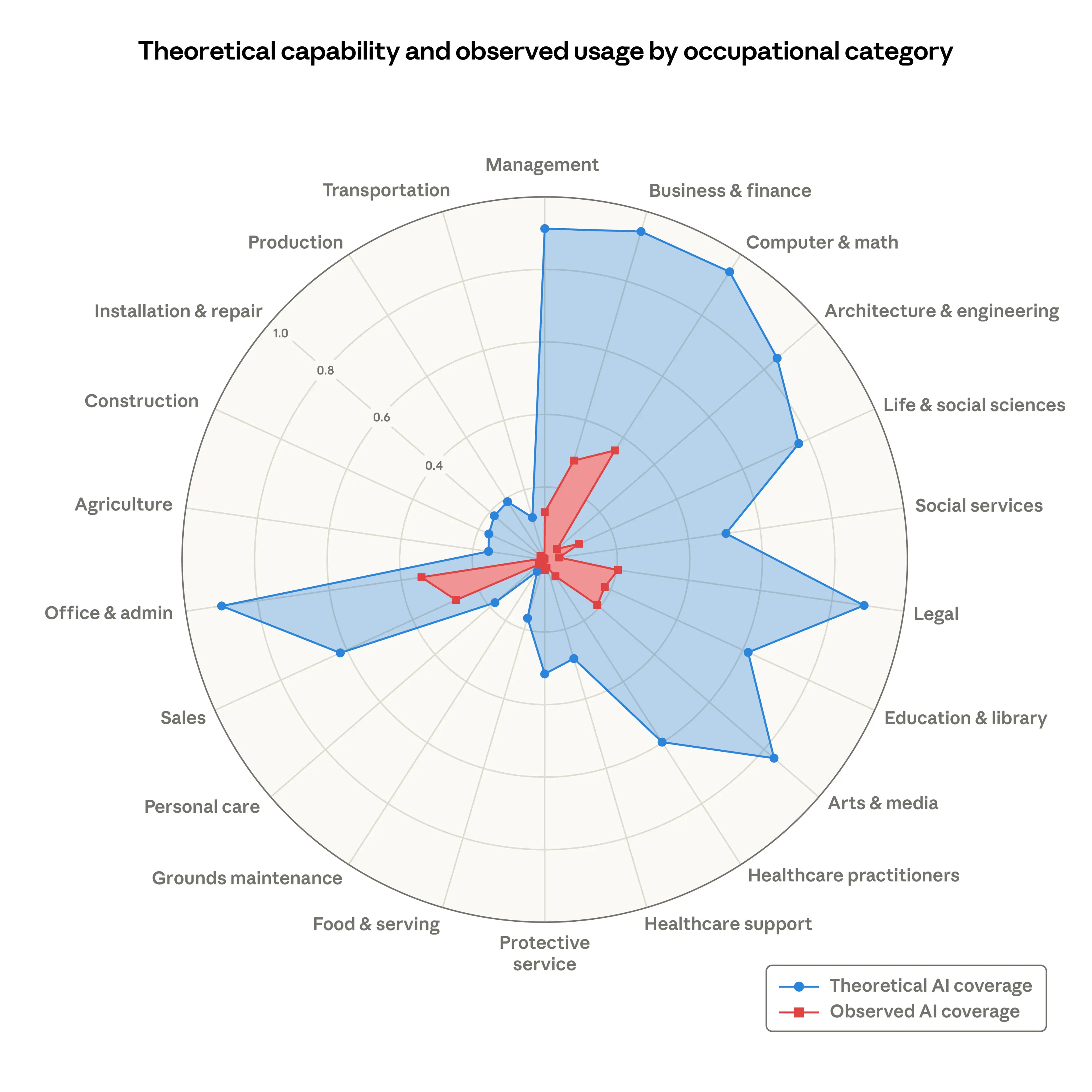

By now, I’m sure everyone has seen Anthropic’s graph around AI coverage by industry and profession. Some important caveats:

Theoretical AI coverage does not mean future AI coverage. It means what current models could theoretically cover today.

The more I look at this, the more I think it’s reductive, which in turn helps clarify the opportunity.

But it is still a great place to start. Here’s my heuristic from the graph:

First, if theoretical model capability is greater than observed AI usage today, research should specialize in agent ergonomics

By agent ergonomics, I mean the tools, sequential reasoning, and environment that the model interacts with.

In other words, a capability overhang means two things:

There is likely a product gap in deploying models.

The harness around the agent is inadequate for the length of task in the vertical.

As a result, research organizations are responsible for determining exactly where the harness and agent are inadequate and subsequently enabling product organizations to fully focus on the user ergonomics around the product.

The focus here is on evaluations, environments, and tool calling, with a special eye toward determining where the agents begin to fail on sufficiently long-horizon tasks.

If there is a current model capability gap and the work should be addressable via software, research teams should focus on data and RL

This is where a dedicated organization to manage research vendors pays off, in my view.

There is a litany of problems inside any vertical that are mostly the result of models lacking verifiability in the domain, and where the problems are sufficiently multimodal rather than just text-based.

These can become some of the most durable revenue streams for vertical SaaS companies as a result, but they demand commandeering data and likely performing RL in order to experience the payoff.

I have an ever-growing list of these that shall remain secret for now. Suffice it to say, the number of problems that we have spent adequate RL on is sufficiently low that hundreds of millions per vertical in revenue is lying in the gutter waiting for vertical SaaS companies to pick up the crown.

Lastly, if total usage and theoretical model capability are both growing, research organizations should spend their time on cost fidelity

Inference is expensive. What should your product organization do when a product has rapid uptake but the margin profile is less than ideal?

Wouldn’t it be nice to hand this problem off to a research organization to deliver cost improvement through RL? It would be.

Lastly, I’ll say this: plenty of vertical SaaS companies touch physical-world operations where sensors and robotics are going to further expand the SAM of labor.

While it is still too early for research organizations to focus too heavily on this problem, future-facing executives should keep an eye on the trendline around rapid physical AI improvement and be situated to take advantage of it the moment the physical world becomes tractable.

We aren’t there yet, but it is certainly coming. The EV of a research organization as this moment approaches will become even higher.

In short, vertical SaaS companies of scale have an unfair advantage with their current revenues: they can become the research organizations that define the frontier in their industry.

The dilemma is how to do this while managing an existing product and business alongside model capabilities that can cannibalize revenue.

Most companies cannot afford to wait, given the rise of so many vertical AI companies and forward-deployed efforts committed to eating all of your software revenue and the labor budget.

Research organizations are not just a plausible path forward. They may become part of the organizational transformation that enables vertical SaaS companies to grow at disproportionate rates going forward.

If you’re exploring this, please reach out.